Anyway, as usual, a digression (or two), even though I haven't even mentioned the main topic.

Brexit

It's a little late to be talking about this, but this is what I was thinking throughout this 'panic'. Of course, like everyone else, I was terrified when the vote came. I never really put much thought to it either way, but when I saw the markets going nuts, I was terrified.

But then I thought about it for a second. OK, so the Brits want out. Fine. Capex and business might slow down for a while as there is uncertainty that wasn't there before; can we build a plant in Britain or not? Do we have to move to continental Europe? Will banks have to move or not?

Two things came to mind when thinking about this. First of all, if you look at all the major tops, markets rarely make a top on some specific news like this. This just felt like fiscal cliff and other mini-panics we've seen in the recent past.

I couldn't imagine, that 20 years from now, that we would be sitting here and looking at a long term S&P 500 chart and go, "see here? That's the high of 2016. Things were OK until Brexit and that was it. It was all over...".

No matter how hard I tried to imagine that, I couldn't.

Second of all, yes there is short term uncertainty, just like the fiscal cliff, end of QE, 9/11 or whatever. But if you look out over five or ten years, how much economic impact is Brexit going to have? People are still going to eat, travel, buy cars and whatnot. Sure, things may be time-shifted due to uncertainty. Maybe someone holds off on expanding capacity in England until things are more clear. Maybe things will shift geographically. Maybe Nissan closes a factory in England and opens one in Germany instead.

Over time, things will be made and consumed. In five years, I don't know if you'd be able to tell by looking at most company income statements and balance sheets what happened.

Over time, things will be made and consumed. In five years, I don't know if you'd be able to tell by looking at most company income statements and balance sheets what happened.

And if that is the case, who cares? The market will understandably go down as people take risk off due to short-term uncertainty, but that doesn't have anything to do with intrinsic value of great businesses five years out.

Also, as is often the case with these things, the situation is dynamic. If you analyze the situation statically, then Brexit can be disastrous in many ways. But it is a dynamic situation. We have to remember that the Europeans need the Brits too. They can't just say, OK, fine. Leave. And no trade. So people will have to work to minimize the damage. Companies are not static, linear organizations. They change and adapt to the situation (well, at least the good ones will).

And not to mention the tendency in some situations for an over-reaction; for example, central banks/governments may, out of fear, overcompensate for the potential negative economic pressure. And who knows, that might actually end up being bullish.

So, after thinking about all of that, I chose to ignore Brexit, even though people I respect were saying that this is serious and is a big deal that will cause a huge crisis. You know, it's still early so it might. Who knows. But this is not the sort of thing I think I have an edge in predicting.

Alternative/Market Neutral Funds

Here's the other thing I've been thinking about again recently. As you know, it's been a peeve of mine for years; mutual funds that try to tactically time the markets and make money in 'all' markets. I guess there are some that can do it well over time, but most don't.

I guess what is surprising to me is that some fund managers allocate short market positions as if it were an asset class. For example, you have funds that think the market is overvalued so they are short the market. OK, for macro hedge funds that makes sense as they are active traders and manage their risk. If they are wrong, they get out and try again later.

But when you apply this sort of thing with an asset allocation mindset, then you end up short for years and have terrible performance.

OK, that's fine. But here's the part I don't get. If stocks are overvalued, say, at 20x P/E, I can see how some may reduce their exposure, go to cash or bonds or whatever.

But if you go short, just because expected returns are low, then your expected return on that short position is still negative, even though it's a small negative. If you think expected returns for stocks is a low 2-4%/year going out, why on earth would you short the S&P 500 for an expected loss of 2-4%/year?

That makes no sense to me.

Anyway, it's just another thing that has been baffling me recently. Again, this doesn't apply to the macro hedge funds as they are active traders. They don't go short and just sit on it for years (well, some actually do that but still manage their risk well enough to make money).

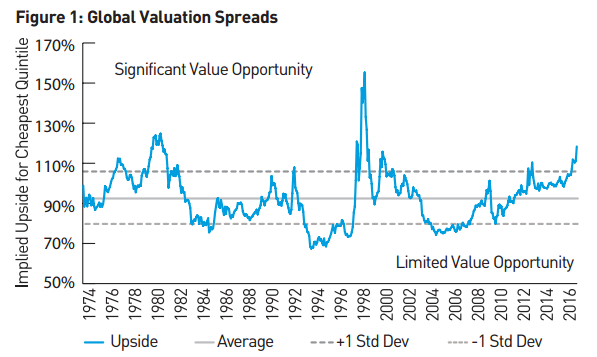

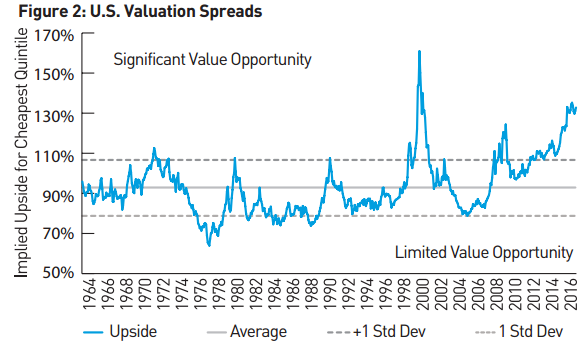

Valuation Spreads

OK, so to get to the original topic of what this post is about. I really enjoy the research by Pzena Investment Management. I keep referring to them but I don't own any funds they manage, nor do I own the stock. And I don't know anyone that works there either, just to be clear as it might seem like I'm promoting them.

Anyway, check these charts out. They are sort of mind-blowing. And for value investors, very exciting to see.

Make sure to read the whole report here: Pzena 2Q commentary

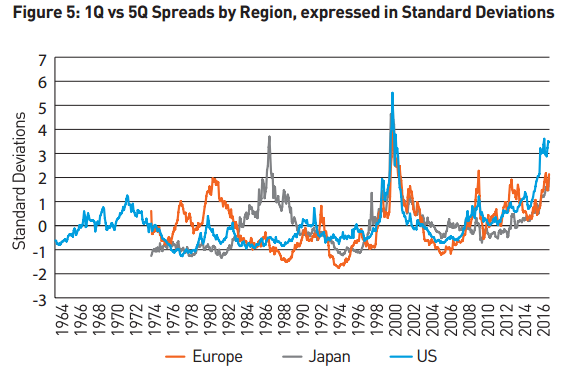

The charts below are the valuation of the bottom quintile stocks compared to the average (or equal-weighted composite valuation). The higher the figure, the cheaper the cheapest stocks are compared to the average. Figure 5 shows the same but compares the cheapest stocks to the most expensive.

You will see that the spread is at historically high levels. That's kind of amazing. This is very, very interesting considering the big boom now in 'passive' strategies. Does this look like an environment where you would want to invest passively?

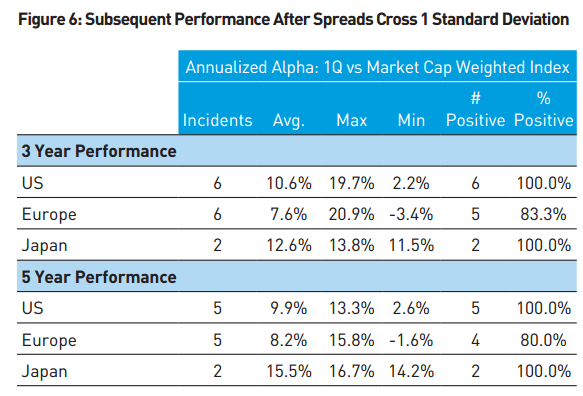

OK, so up to here you might say, so what? That's great for long/short equity funds. But what about long-only value guys? Well, Pzena has already thought of that, and here is how the bottom quintile (cheap) has performed three and five years after the spread widens.

.

Alpha may not be too encouraging if you are a big bear. 10% alpha could still be a 20% loss if the market is down 30%.

How to Play It?

Of course, the obvious way to play it is to stick with cheap stocks. That is always a great idea, but it seems like it's a really, really great idea now.

But, there is another interesting idea here. Most of you have probably already thought of this.

You know that one of my favorite authors and fund managers has a company running mutual funds. Yes, Joel Greenblatt. I'm so predictable.

And yes, I know, the Gotham Funds have not been doing so great performance-wise. But if you see the above charts, it's easy to see why: expensive stocks have been getting more expensive and cheap stocks are getting cheaper.

Now, I am not a big fan of mean-reversion when looking at the market. I do believe in mean-reversion to a point. But that has lead people astray for decades. For example, people waiting for mean-reversion of P/E ratios in the stock market have been waiting for 20, 30 years. Dividend yields too, for even longer. People waiting for interest rates to mean-revert have been waiting for decades too.

But some things do mean-revert much more reliably. I would say volatility is one of those things. Volatility can't and won't stay above 20-30% for any length of time.

Another, I think, are the above valuation spreads.

If you think those charts will keep going up like that, then invest in momentum funds and chase the hottest funds and you'll be fine (if those charts keep going up exponentially like that).

But if you think things will mean-revert, then piling into value stocks seems like a great idea.

If you want to be market neutral and 'safe', then the Gotham long/short funds are probably perfect; it may be the best time, ever, to invest in the Gotham long/shorts.

Gotham's long/short funds mechanically (with human overlay, I hope) short the dearest and buy the cheapest stocks. True, they are not using P/B ratios, so investing in a Gotham long/short fund would not be the same as trading those charts above. But I would imagine they would be correlated.

Gotham Funds

So, returns so far at Gotham haven't been so great. Not so bad either, but not so exciting. The charts above sort of indicate why that was so, so far...

...but things may be starting to look better...

Forgot to post this more updated table when I initially posted this. Year-to-date looking much more interesting. These returns can really take off on any big mean-reversion of valuation spreads...

So, if you think the above charts will keep going up, and more and more money will keep going into passive strategies, then ignore all of this, maybe.

But, if you think that the above chart rubber bands will snap the other way, eventually, and that active managers will start to outperform passive strategies etc., then maybe think about investing in some good value managers, long/short equity funds etc

Here is their webiste: Gotham website.

Here is their webiste: Gotham website.

I think today, this is one of the most contrarian bets you can make!

Oh, and I don't know anyone at Gotham either...