Sometimes, some investors just buy or own stuff that just resonates with me, like that time Nehal Chopra of Ratan Capital was on CNBC talking about Post Holdings and Charter Communcations. I owned (and still own) both of them. Apparently, Chopra dumped POST when it tanked but bought back recently. I rode it all the way down without selling anything and am nicely in-the-money on it now.

At the time, I had no idea who Chopra was.

This is sometimes why I post about certain investors. If they do something that interests me, I will make a post about it. And if it happens three times in a row, well, so be it. Surely, other investors have made more interesting buys recently. This is just what jumps out at me. By the way, I don't own BAM, SCHW or AME.

Anyway, AMETEK (AME) has been mentioned here in the past (by readers) as an outsider-CEO-type company; growing through acquisitions etc. Maybe you can call it a DHR-like company. I guess "outsider-CEO-like company" might not sound so great now after VRX, but whatever.

And by the way, I know it's been a while since I posted. I never make a post and then say, OK, I'm going to take a break for a month or two from blogging. It's just that time passes and then it's like, wow, I haven't posted in more than a month! Well, all sorts of things happen, some travelling, obsession with other things etc. But my main thing is still investing; it's just that sometimes time flies without me having made a post even when some ideas pop up (and I never bother to make the post for one reason or another).

Simpson Buys Big

So check this out. Simpson had no AME shares earlier this year (and never showed up in any 13-F for SQ Advisors recently).

Number of shares of AME in SQ Advisors' 13-F:

3/31/2015: 0

6/31/2015: 1.8 million

9/31/2015: 8.1 million

So that's kind of huge. The 13-F as of September-end showed $3.0 billion in U.S. stocks, and more than 14% of the portfolio in AME (this excludes cash and other assets that are not U.S. listed stocks).

Lou Simpson Portfolio

My last couple of posts related to Simpson were about BAM and SCHW, and AME is even bigger than those. It's also interesting that Simpson added to VRX in September, but this was before the real crash in the stock. I wonder what he did after that. It is interesting how Munger can really despise this company and Simpson can like it enough to make it such a large holding (he has owned it since (at least) 2011 and actually owns more shares now than in 2011; 2 million shares as of September 2015 versus 1.2 million back in 2011).

AME

AME has been run by Frank Hermance (now aged 66 or so) since 1999. He became President and CEO in September 1999 and Chairman and CEO in January 2001. AME aims to double the size and profitability of the company every five years. 1/2 to 2/3 of their growth is to come from acquisitions.

From their 10-K, this is what they do:

Products and Services AMETEK’s products are marketed and sold worldwide through two operating groups: Electronic Instruments (“EIG”) and Electromechanical (“EMG”). Electronic Instruments is a leader in the design and manufacture of advanced instruments for the process, aerospace, power and industrial markets. Electromechanical is a differentiated supplier of electrical interconnects, precision motion control solutions, specialty metals, thermal management systems, and floor care and specialty motors. Its end markets include aerospace and defense, medical, factory automation, mass transit, petrochemical and other industrial markets.

Competitive Strengths

Management believes AMETEK has significant competitive advantages that help strengthen and sustain its market positions. Those advantages include:

Significant Market Share. AMETEK maintains significant market shares in a number of targeted niche markets through its ability to produce and deliver high-quality products at competitive prices. EIG has significant market positions in niche segments of the process, aerospace, power and industrial instrument markets. EMG holds significant positions in niche segments of the aerospace and defense, precision motion control, factory automation, robotics, medical and mass transit markets.

Technological and Development Capabilities. AMETEK believes it has certain technological advantages over its competitors that allow it to maintain its leading market positions. Historically, it has demonstrated an ability to develop innovative new products that anticipate customer needs and to bring them to market successfully. It has consistently added to its investment in research, development and engineering and improved its new product development efforts with the adoption of Design for Six Sigma and Value Analysis/Value Engineering methodologies. These have improved the pace and quality of product innovation and resulted in the introduction of a steady stream of new products across all of AMETEK’s lines of business.

Efficient and Low-Cost Manufacturing Operations. Through its Operational Excellence initiatives, AMETEK has established a lean manufacturing platform for its businesses. In its effort to achieve best-cost manufacturing, AMETEK has relocated manufacturing and expanded plants in Brazil, China, the Czech Republic, Malaysia, Mexico, and Serbia. These plants offer proximity to customers and provide opportunities for increasing international sales. Acquisitions also have allowed AMETEK to reduce costs and achieve operating synergies by consolidating operations, product lines and distribution channels, benefitting both of AMETEK’s operating groups.

Experienced Management Team. Another component of AMETEK’s success is the strength of its management team and that team’s commitment to improving Company performance. AMETEK senior management has extensive industry experience and an average of approximately 23 years of AMETEK service. The management team is focused on achieving results, building stockholder value and continually growing AMETEK. Individual performance is tied to financial results through Company-established stock ownership guidelines and equity incentive programs.

Business Strategy

AMETEK is committed to achieving earnings growth through the successful implementation of a Corporate Growth Plan. The goal of that plan is double-digit annual percentage growth in earnings per share over the business cycle and a superior return on total capital. In addition, other financial initiatives have or may be undertaken, including public and private debt or equity issuance, bank debt refinancing, local financing in certain foreign countries and share repurchases.

AMETEK’s Corporate Growth Plan consists of four key strategies:

Operational Excellence. Operational Excellence is AMETEK’s cornerstone strategy for improving profit margins and strengthening its competitive position across its businesses. Operational Excellence focuses on cost reductions, improvements in operating efficiencies and sustainable practices. It emphasizes team building and a participative management culture. AMETEK’s Operational Excellence strategies include lean manufacturing, global sourcing, Design for Six Sigma and Value Engineering/Value Analysis. Each plays an important role in improving efficiency, enhancing the pace and quality of innovation and cost reduction. Operational Excellence initiatives have yielded lower operating and administrative costs, shortened manufacturing cycle times, higher cash flow from operations and increased customer satisfaction. It also has played a key role in achieving synergies from newly acquired companies.

Strategic Acquisitions. Acquisitions are a key to achieving the goals of AMETEK’s Corporate Growth Plan. Since the beginning of 2010 through December 31, 2014, AMETEK has completed 26 acquisitions with annualized sales totaling approximately $1.4 billion, including five acquisitions in 2014 (see “Recent Acquisitions”). AMETEK targets companies that offer the right strategic, technical and cultural fit. It seeks to acquire businesses in adjacent markets with complementary products and technologies. It also looks for businesses that provide attractive growth opportunities, often in new and emerging markets. Through these and prior acquisitions, AMETEK’s management team has developed considerable skill in identifying, acquiring and integrating new businesses. As it has executed its acquisition strategy, AMETEK’s mix of businesses has shifted toward those that are more highly differentiated and, therefore, offer better opportunities for growth and profitability.

Global & Market Expansion. AMETEK has experienced dramatic growth outside the United States, reflecting an expanding international customer base and the attractive growth potential of its businesses in overseas markets. Its largest presence outside the United States is in Europe, where it has operations in the United Kingdom, Germany, France, Denmark, Italy, the Czech Republic, Serbia, Romania, Austria, Switzerland and the Netherlands. While Europe remains its largest overseas market, AMETEK has pursued growth opportunities worldwide, especially in key emerging markets. It has grown sales in Latin America and Asia by building, acquiring and expanding manufacturing facilities in Reynosa, Mexico; Sao Paulo, Brazil; Shanghai, China; and Penang, Malaysia. AMETEK also has expanded its sales and service capabilities in China and enhanced its sales presence and engineering capabilities in India. Elsewhere in Asia and in the Middle East, it has expanded sales, service and technical support. Recently acquired businesses have further added to AMETEK’s international presence. In recent years, AMETEK has acquired businesses with plants in Germany, Switzerland, the United Kingdom, Serbia and China as well as acquired domestically located businesses that derive a substantial portion of their revenues from global markets.

New Products. New products are essential to AMETEK’s long-term growth. As a result, AMETEK has maintained a consistent investment in new product development and engineering. In 2014, AMETEK added to its highly differentiated product portfolio with a range of new products across each of its businesses.

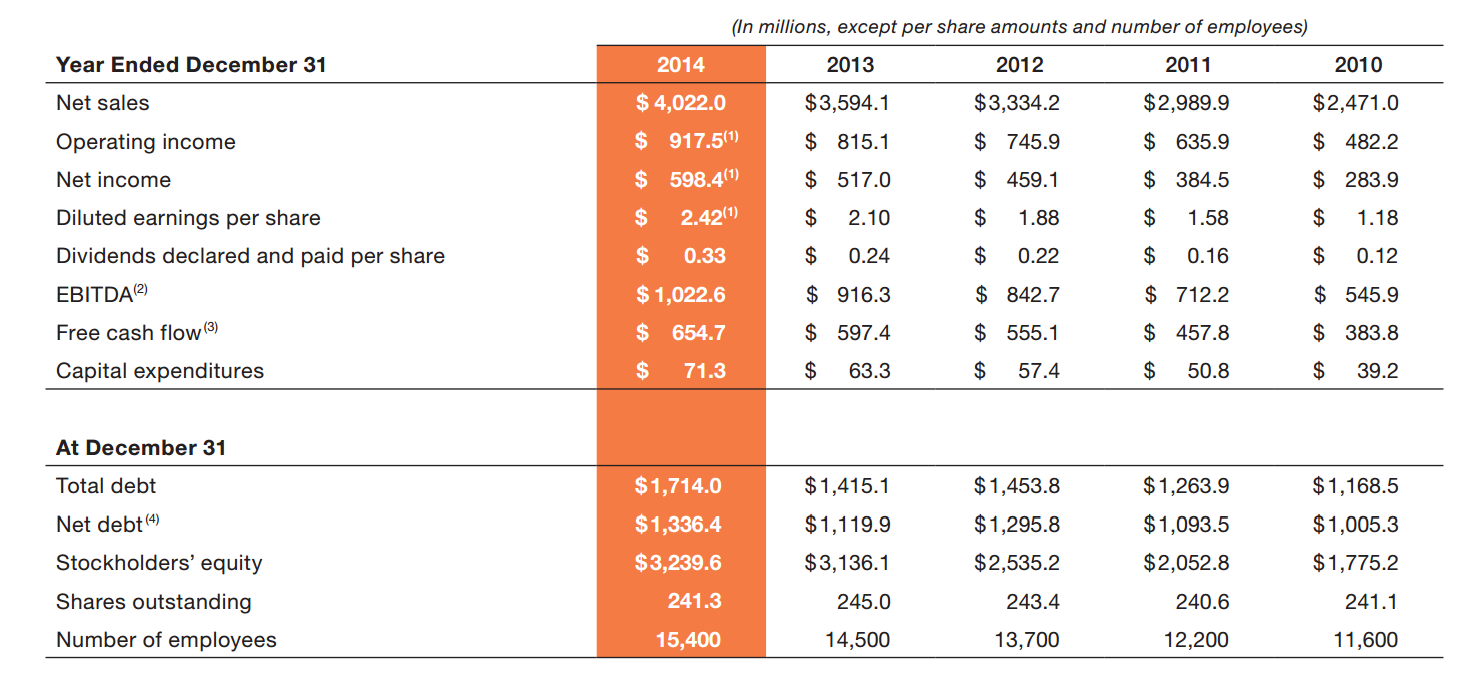

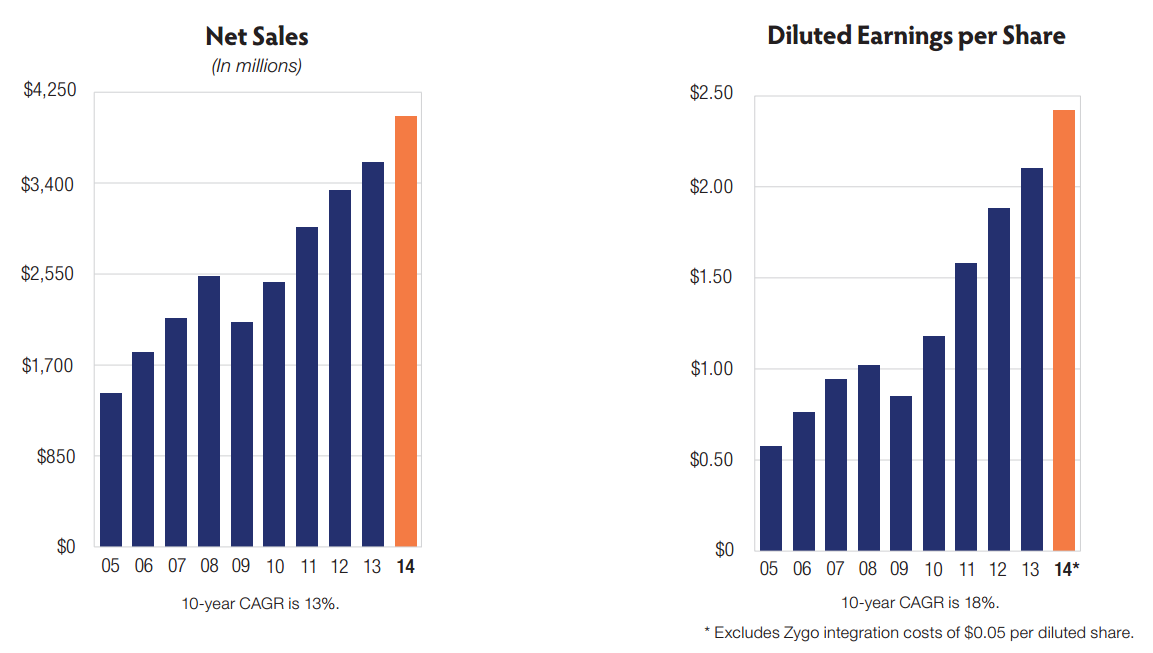

And from the annual report, a snapshot:

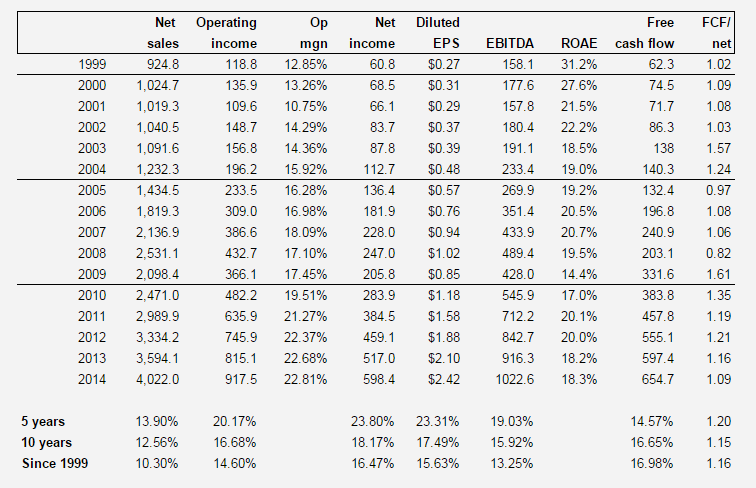

It looks pretty impressive. Nice growth, and new highs after the 2008/2009 recession pretty quickly. I dug up some figures going back to 1999 when Hermance became CEO to see how he has done, and it is pretty impressive:

Financial Summary of AME since 1999

Net sales grew 10%/year since 1999 while operating income grew around 15%/year, and EPS around 16%/year.

As with DHR, free cash flow has been higher than net income throughout the period by around 1.2x.

The interesting thing about AME is that these figures are not "adjusted" or anything like that. Unlike, say, VLX, AME's EPS is plain EPS.

As of the third quarter, guidance for the full year 2015 was $2.55/share, up 5% over 2014. With the stock at around $54/share, it's trading at a P/E of around 21x.

Conclusion

AME does seem to be facing some macro headwinds. Oil and gas hasn't been too much of an issue as they don't have that much exposure to upstream, but slowing growth in Asia and emerging markets are holding back their growth this year and probably into next year. So there is some risk there.

The stock is certainly not for cheapskates at 21x P/E, but they do have good free cash flow conversion and growth potential. Their operating margins are higher than say, DHR or CFX too (with similar business models). AME isn't leveraged at all, either, with long term debt of $1.6 billion against 2014 EBITDA of $1 billion. With the junk bond market tanking and rates going up, this may be a good thing.

There are plenty of 20+ P/E stocks with very little growth prospects (and the whole market at close to 22x P/E), maybe this is not a bad idea. Historically, AME has traded at around 20x P/E.