Not long after my post on Alleghany's (Y) investor day, Weston Hicks presented at a Merrill Lynch conference. I think it's the first time I've ever heard him speak so it was pretty interesting (I wasn't there; I just listened to the replay).

You can get a link to the presentation at Y's website: Presentation

For anyone interested in Y, it's definitely worth a listen. It's pretty short too (unlike, say, the JP Morgan investor day; not complaining about that. The more info there is, the better!).

Hicks talked about the history of Y. I guess it sort of shows us why they are so conservative (they survived this long because of that conservatism).

Here are some interesting slides from the presentation:

Y CEO's tend to be CEO's for a long, long time. This obviously is important as it leads to CEO actions that are long term in nature.

...and they have been in various businesses over the years according to what made sense at the time:

...and here are the keys to Y's success:

Burns is right, there is nothing wrong with getting rich slowly. I suppose that was thrown in there to counter views that Y is too boring and conservative (who said they are boring and too conservative? Did I say that?). But yes, there is nothing wrong with being a tortoise. As Buffett says, to finish first, one must first finish.

And here is the value proposition of Y which applies to other Berk-alikes:

And here's an interesting quote that he showed during the presentation which went into the annual report too:

And the evolution of Y over the past decade (pretty much since Hicks took over):

As I mentioned in my last recent post, the investment team has been regrouped and renamed (Roundwood is a new name; Roundwood is named after Roundwood Manor, the home of the Alleghany Corp founders).

One year doesn't prove anything, but the equity portfolio performed well in a big year for the stock market despite being only 80% or so invested. I do like that they will keep the number of positions below 25 with low turnover. That seems to me a good idea. It did say in the annual report that Y has invested with Jack Liebau before with good results.

...and here's the private business group:

Hicks jokingly said "no comment" about the last time Y underperformed the S&P 500 index on a five-year basis (which was in 2007). Y underperformed dramatically in the five years through 2013. I don't think too many rational investors care about that since the five year return on the S&P 500 index is obviously a result of the financial crisis low and quick recovery thanks to the Fed and not representative of what the S&P 500 index can do going forward.

Y's stock price has barely outperformed the S&P 500 index over the past decade, and their book value outperformed by only 1.1%/year. That's not that exciting, but as Y explains later in the annual report, they have achieved this with a much lower risk profile.

2013 Annual Report

Y grew book value per share +8.9% to $412.96/share in 2013. The five year increase in BPS was +9.1%/year versus +17.9%/year for the S&P 500. But we'll get to the discussion about this a little later.

But first, some interesting cut and pastes from the letter to shareholders:

I like the way they present change in shareholders' equity. It's easy to understand what drove the change in net worth in the past year:

And here's a new table that breaks out ROE and book value growth contribution by group. This is a nice way to present it. We can see the investment return figures separately too so we get a good idea on what is driving the growth at Y.

Whale Trade!?

OK, I'm kidding about a whale trade, but you'll see what I mean in a second. There was a very interesting change in this year's annual report. As I've said in other posts (unrelated even to Y), Y has over the years explained that they seek equity and private business investments to sort of hedge their interest rate exposure as they saw inflation as inevitable.

But this year, I think for the first time, they said they are worried about deflation. There is talk about demographics, world trade, possible spike in energy prices causing a recession, robots and other deflationary forces (not to mention too much debt around the world).

So they have an equity portfolio as they worried about inflation (well, that's not the only reason why they own equities). The equity portfolio was sort of an inflation/interest rate hedge. And now, they are worried about deflation, so they went out and bought zeroes to hedge against deflation. So that's kind of like hedging your hedge, isn't it? Isn't this how J.P. Morgan got into trouble? They had a hedge on, but then they had too much of a hedge so they put on a hedge against their hedge. And it turned out their hedge against their hedge wasn't really a good hedge, and that sort of blew them up.

I wrote about the risk of increasing complexity in a portfolio; it happens all the time. I called it the Rube Goldberg portfolio (read here).

In situations like this, sometimes what happens is that you get surprise inflation and the stock market tanks along with the zeroes. What can go wrong usually does in the financial markets! Inflation driven by economic recovery would be OK, but it can also be driven by exogenous events. Who knows what that might be.

But OK. The whale trade comparison is overkill here. Insurance companies routinely manage their duration according to interest rate expectations (as do banks with their ALM) so this is just a part of that, I suppose. Let's call it a tail hedge (hedge against fat tail events).

I wonder what out-of-the-money, long dated call options on zeroes are trading at? Maybe that would've been a low cost tail hedge. With so much expectation of rate normalization, I can't imagine them being overpriced.

Anyway, moving on.

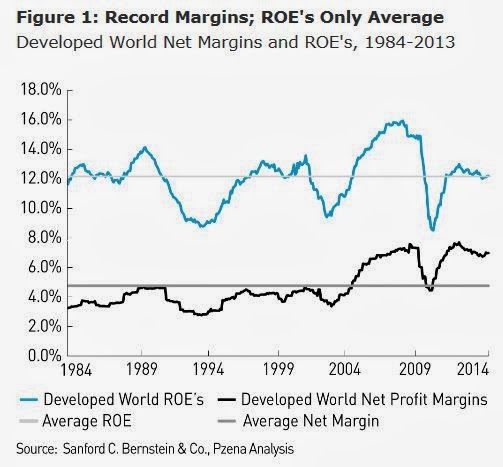

Equity Valuations

I talk about equity valuations here every now and then, but I don't really obsess over it. I actually don't care as those things are only meaningful at the extremes. If I see extreme valuations and many signs of speculation/bubble, then of course I get a little worried. But I still focus on individual companies so don't worry too much about it.

Having said that, I am interested in what others have to say about valuation, and Hicks does mention it in his letter:

I too worry about unsustainable profit margins sometimes, but I notice that a lot of companies have exited commodity businesses and are moving more into specialty, higher margin areas. This is why I think it's really important to look at this stuff on a company by company basis.

Y's equity portfolio did well:

Risk-Adjusted Return of Y

So here's an interesting take on Y's performance over the past decade:

This is an interesting analysis. I think much of Y's book is marked to market unlike, say, BRK, which has a large portfolio of businesses that is not. In that sense, this may be a fair analysis, at least in terms of comparing Y to the S&P 500 index. But then this would invite similar comparisons to other companies; how does Y fair against them using the same metric? I bet Markel would look pretty good. JP Morgan would probably look pretty good too.

The letter concludes:

Conclusion

So, just within the past few weeks, we get to see much more of Y. I think the 2013 letter is one of the best for Y, and the presentation material from the investor day and Merrill Lynch conference is really good too.

Stanley Druckenmiller ranted about how hedge funds these days talk about "risk-adjusted" returns. He thinks that's really pathetic; in his day, they were expected to earn 20-30% or more year in and year out no matter what the markets did. These days, high fee funds earn single digit returns and tell people that the returns are good on a "risk-adjusted" basis. He calls that nonsense.

So looking at it that way, it looks sort of like Y pulled out this "risk-adjusted" thing to set itself apart from the S&P 500 index. So if some people criticize that, it's understandable.

But I also do get Y's point of view. They are and have been very conservative in their management over the years (read their letters to shareholders). So it's true that it is not bad that they kept up with the market (over ten years) despite what I would call an overly conservative stance.

And to illustrate the value of their conservatism, Hicks reached back into the history of Y; they have survived for so long because of it. If that's too boring, too bad. Better boring than dead.

I really like what is happening there, though. I have argued in the past that companies that don't earn a ROE higher than 10% isn't worth much more than book value and I still sort of feel that way. But if the ROE is close to 10% conservatively managed with upside according to normalization of interest rates and other things, then maybe it's not so bad. We are not talking about a business that is taking a lot of risk and reaching for a 10% ROE. It's a conservatively managed 7-10% in a 3% interest rate world with possible upside depending on how things develop. That's a big difference. In the fixed income world, you would have to dip down into the lower credit ratings to get a 7-10% return.

So in that sense, Y is not a bad idea at under BPS.