The insurance business is only ramping up now so there isn't much to chew on in terms of analysis. Like GLRE, the key is going to be underwriting profits (or at least break-even) and investment returns. If TPRE can generate float at a low cost and Third Point can generate some decent returns, this can be a great investment.

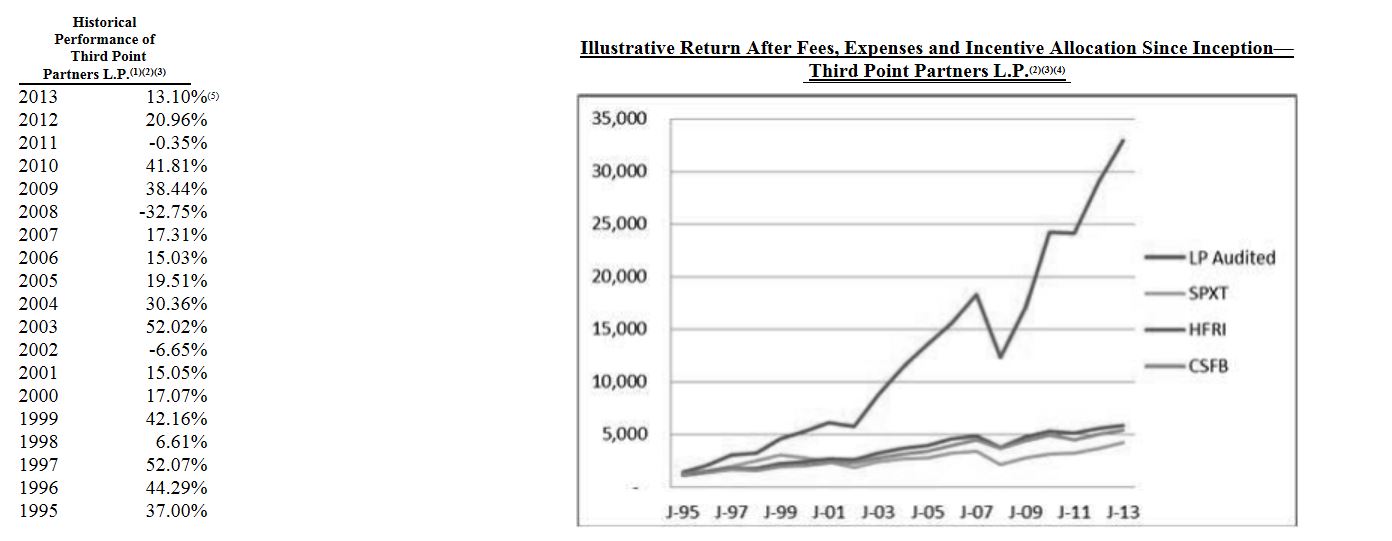

Third Point Investment Returns

Of course, the big question is how the insurance operation is going to turn out. The investments will be managed on the same basis as the hedge fund and the historical returns are pretty good. Third Point LLC has AUM of $13.2 billion (as of June 2013) and has returned 21.0%/year from June 1995 through December 2012.

The five and ten year returns (through December 2012) were:

Five year: +9.7%/year

Ten year: +17.7%/year

Third Point will own 8.5% of TPRE after the offering. Kelso and Pine Bank will own 26.5% and 13.4% respectively.

Here's a cut and paste from the S-1 that shows the long term performance of Third Point Partners:

Management and incentive fees will be 2%/20%, a standard rate. (GLRE pays 1.5%/20% to Einhorn).

Assuming the offering price is $13.50 (range of $12.50 - 14.50), the proforma book value after the offering comes to $12.41/share (excluding greenshoe). On a fully diluted basis, the BPS comes to $12.17/share (assuming no greenshoe and 7% underwriting spread).

So at $13.50/share, that comes to 1.1x fully diluted proforma BPS. That sounds good to me.

Insurance Risk

There is the question of the insurance business. These hedge funds that start up reinsurers typically go for the low volatility, low tail risk strategies by focusing on high frequency / low severity risks. This is true with GLRE too, as they want to minimize insurance risk and take the risk on the investment side; to the extent that their portfolios are not low risk fixed income like most insurers/reinsurers, they would want less p/l volatility on the insurance side.

I can't say anything to comfort anyone with concerns in the insurance business of these entities (TPRE, GLRE etc.) other than to say that these hedge fund folks have made a career out of managing risk. They may not understand the insurance business as well as people who are actually in the business, but I would imagine that they would know enough (and have the resources to figure out) to get the right people and understand the risk. Things may not look good now for hedge funds with what's going on with JCP (and SHLD), but that may just indicate how tough bricks and mortar retailing is now more than anything about hedge funds.

Of course, this is no guarantee of anything. Even Loew's James Tisch has said in a recent interview that he thinks that some of these hedge funds that start reinsurance companies may be underestimating what the insurance business can lose in a really bad year.

Just because a reinsurer writes a bunch of short-tail, capped risks (like selling deep out of the money put spreads) doesn't mean that they can't blow up. And if the insurance portfolio is managed to eliminate too much risk, there is a question of how much they can earn on such businesses.

So for me, these issues might put a constraint on how much exposure I would want in each of these entities; it is certainly not as rock solid as Berkshire Hathaway (but what is?), but that doesn't mean it can't have an attractive return/risk profile; just don't put 80% of your net worth in it.

For those interested in Third Point but don't care for float leverage, tax free BPS growth (and the insurance risk that comes with it), Third Point Offshore Investors is still trading at a slight discount to NAV in London (TPOU:LN).

Conclusion

At 1.1 or 1.2x BPS, I do think TPRE is an attractive opportunity. I know that there is a big split in the opinions about hedge funds; some people love them, others hate them. I don't have a problem with banks, investment banks or hedge funds (as long as they are doing things that I think I understand; I have no idea how SAC has made such high returns over the years, for example. But Greenlight, Third Point and others seem to be doing things that I feel comfortable with; value investing, event driven trades, value investing with a catalyst, distressed debt and other special situations etc.)

The S-1 does include an overview on the various strategies that Third Point does and it's certainly an interesting read, particularly for those curious about what some of these funds do.

This post is a little light, but I just wanted to get this out as I do think it's interesting. If I have anything to add, I may post followups (and I probably will over time as it lists and more results come in).