Anyway, here are some slides I took from the presentations from their website.

I already mentioned what a great investment opportunity JPM was last fall when it was trading at tangible book value. You can read that here: JPM at Tangible book

Book Value per Share Growth

As I said before, what is truly amazing about Dimon and J.P. Morgan is how they performed during the worst financial crisis in history. Remember, J.P. Morgan was often cited as the first domino to fall in any financial crisis due to their huge derivatives book and exposure to the investment banking business.

But look at the chart/tables on this slide:

From 2006 - 2011, that includes the peak of the bubble and then the collapse in 2008-2009 and recovery which hasn't been completed yet. JPM grew their book value per share at 7%/year during this time, and 9%/year for the past ten years. Again, that *includes* the financial crisis! Tangible book value per share grew 12%/year over this time period and 8%/year over the past ten years.

I know many bank critics will say that they just got bailed out so of course they did well. As I said before, I don't think JPM needed the TARP money. They took it, paid high interest, and then paid it back.

Did JPM need the financial industry to be bailed out to survive? Well, if the whole system collapsed, then yes JPM might have gone down too. But that's what the Fed is there to prevent and that's what they did. I don't think there is anything wrong with that.

Other critics will say that JPM is or was insolvent but of course they didn't lose money because they didn't have to mark their books correctly. Again, I would just say that Dimon is the best and most conservative manager out there and he *hates* mismarked books more than anyone.

And if it was just a simple accounting trick that prevented JPM from going under, then how come Bear Sterns, Washington Mutual, IndyMac, Citigroup, AIG and many others didn't use the same accounting trick to prevent taking losses?

So no, it wasn't an accounting thing or mismarking that allowed JPM to perform well. It was just managed well.

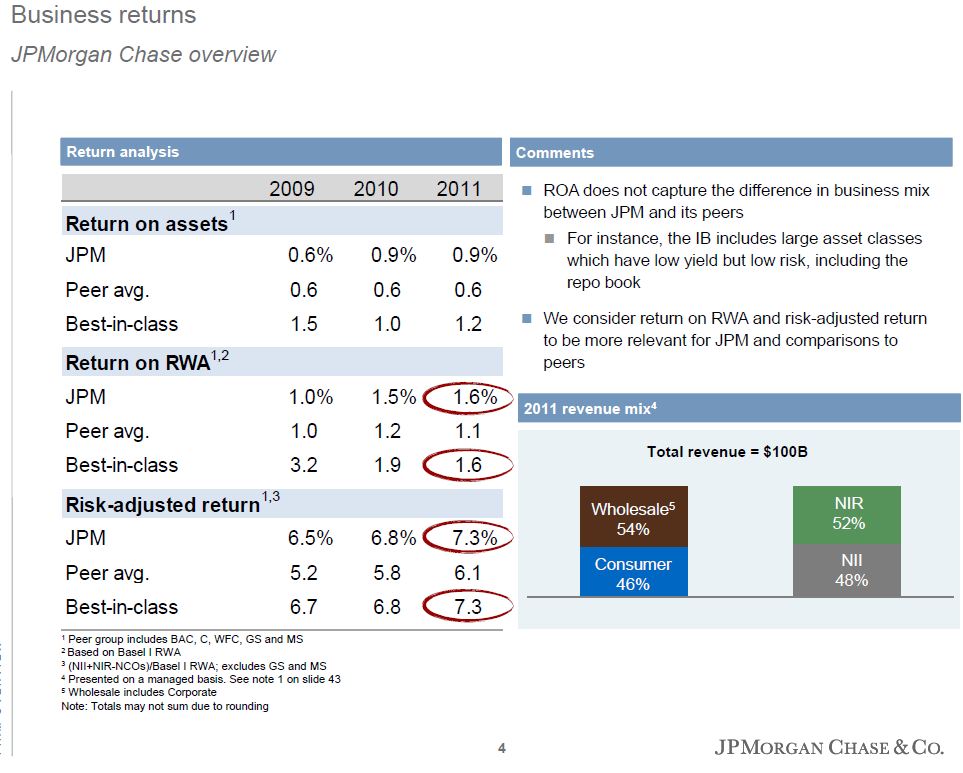

Low Return on Assets?

I think one reason why JPM trades for cheaper than, say, Wells Fargo, is that their return on assets look much lower.

In the slide below, JPM shows that their return on assets is low due to their large exposure in the investment banking business, which is not a loan spread business; much of their assets will show a low return on asset.

Adjusted for these differences, JPM looks much better.

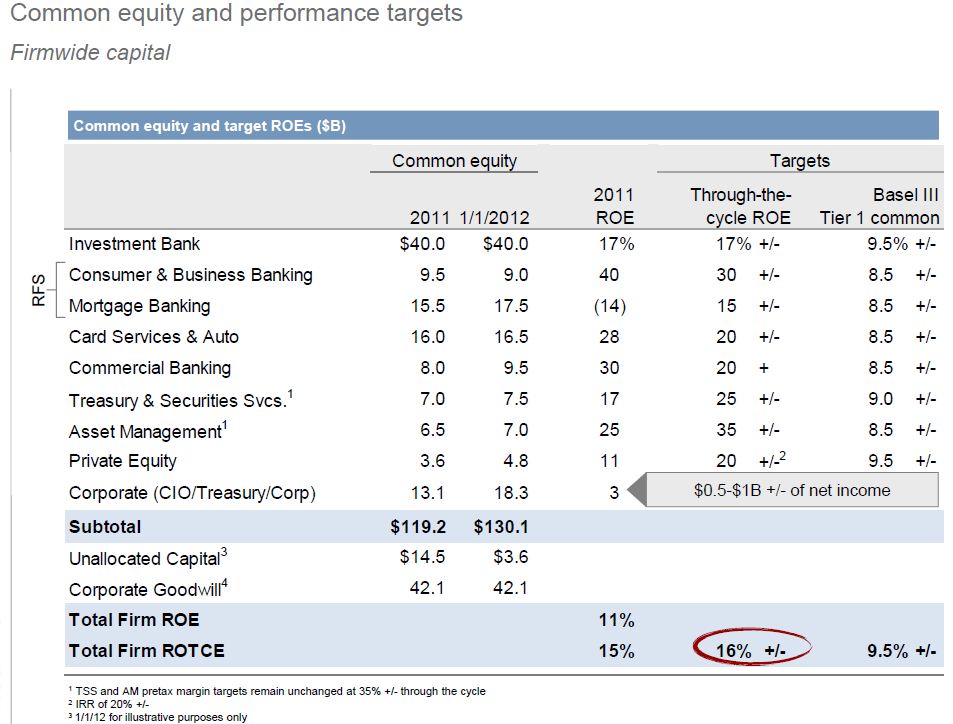

ROE by Business Line

Also, ROE of each of the business lines look really great, and that's amazing when you think about the fact that even the great Goldman Sachs didn't do too well on this metric in 2011.

The investment bank earned an ROE of 17%. Consumer and Business Banking earned an ROE of 40%. It's truly amazing how profitable these businesses are in a time when financials aren't doing too well in general; loan growth is low or non-existent, housing hasn't recovered, the economy is still very slow to improve etc...

JPM continues to invest for growth, so there could be some tremendous operating leverage when more areas of the economy start to pick up, like housing. They have really built up their mortgage business so if housing starts to come back, upside could be substantial in this area for JPM.

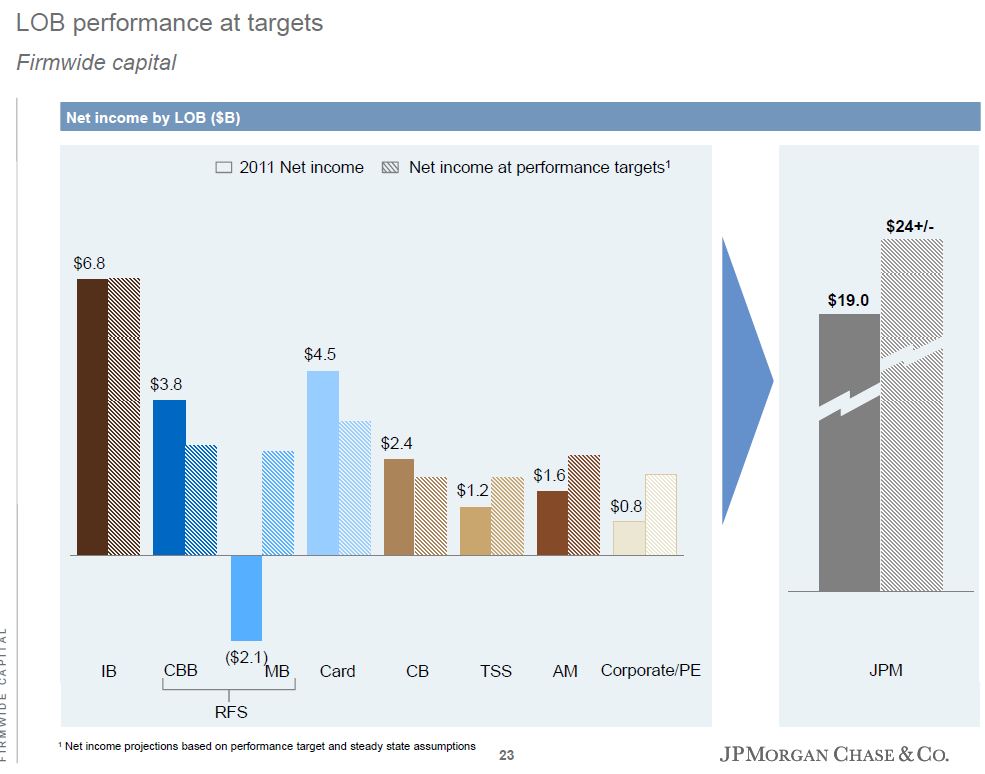

So JPM has performance targets by segment. Assuming each segment achieves it's ROE target, the total net income to JPM would be $24 billion. With 3.8 billion shares outstanding, that comes to $6.40/share in EPS.

Now hold that $6.40/share thought for a later section.

The following bridge, or walk or whatever you want to call it is how JPM can get to $24 billion net income. It includes the normalization of high credit charge offs, mortgage related expenses and things like that but doesn't include any robust recovery in the economy or any such thing. Growth inititiaves only add 4% or so.

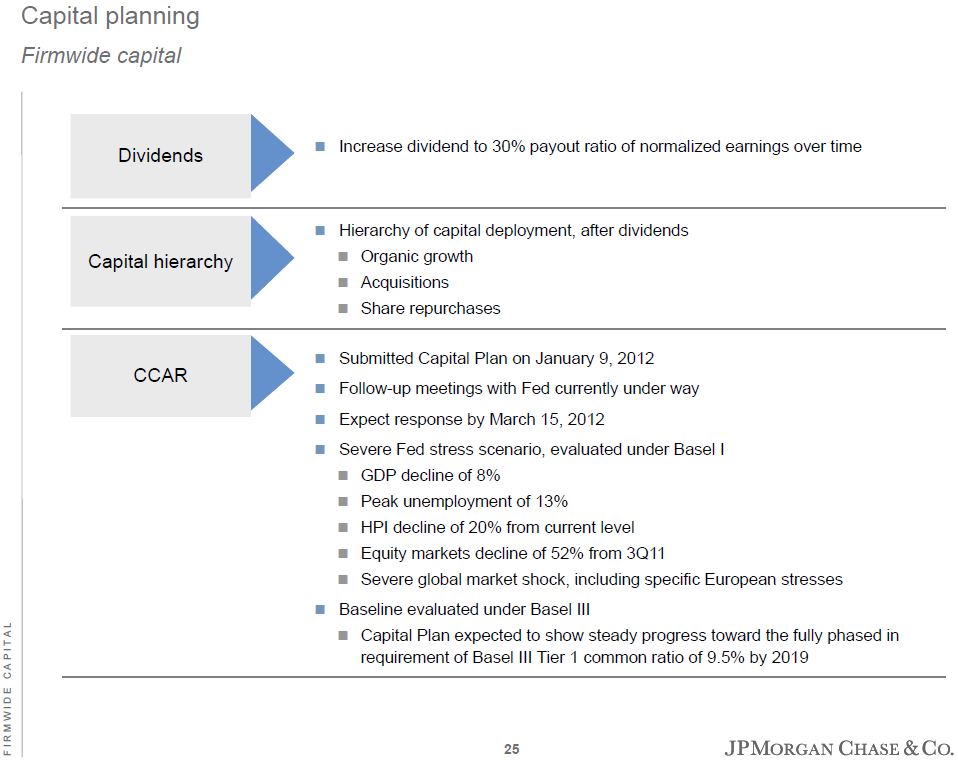

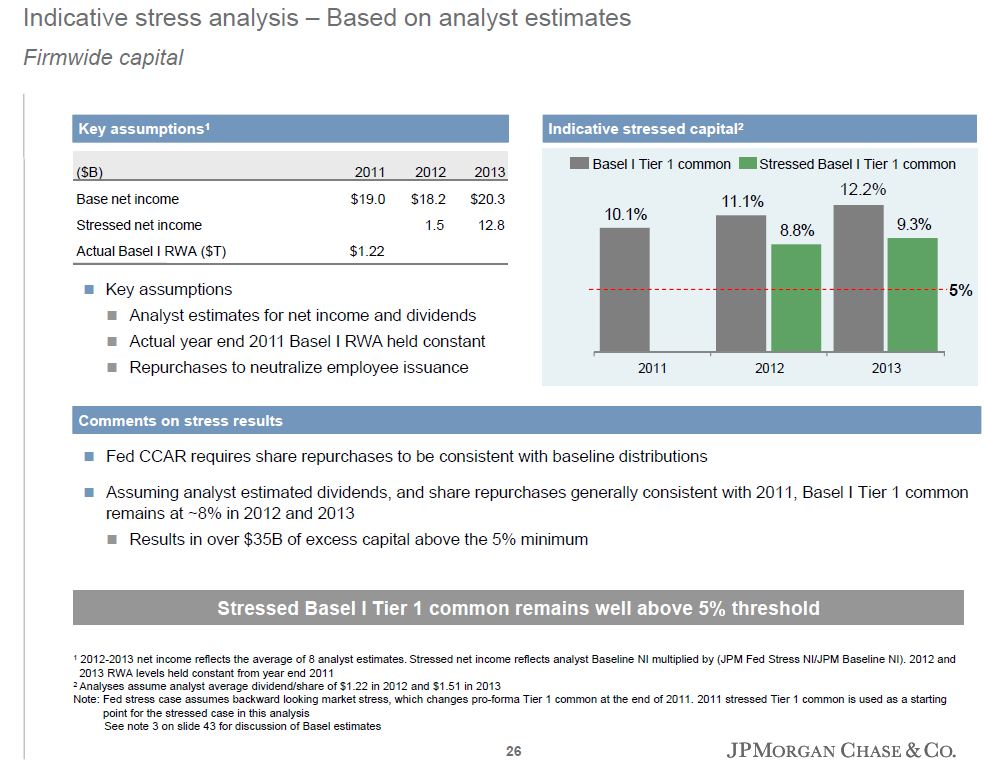

Capital and Stress Test

It doesn't look like acquisitions will be a major thing in the near term as Dimon seemed to suggest that it's off the table for now because he doesn't think it's politically doable now in this environment (where people are calling for breaking up the too-big-to-fail banks).

I think over the next few years, people will be surprised at what Dimon is building now. Many banks are cutting investments to boost profits (like Bank of America?) as Dimon keeps spending to build branches and expand market share. This may not be evident or visible now as housing is still in the dumps, so expanding mortgage operations won't really show results as much as when housing starts to pick up again.

Anyway, the other issue with the banks is the stress test. It's amazing how well prepared JPM was for the last real crisis and they have always been ready for them. So this stress test should be easy for JPM. It is encouraging that even with the above stress test scenario of housing prices going down another 20%, unemployment rate going up to 13%, GDP going down 8% and stock prices going down 50% from their 3Q2011 lows that JPM will have no problem getting through it.

Incredibly, they would get through that crisis with a positive net income. Now, that's a fortress business!

Conclusions

So what does this all mean?

- If you go back to the above $6.40/share EPS based on the lines of businesses achieving their ROE goals, that would put JPM's stock price now 6.3x p/e. That's pretty darn cheap. At 10x p/e, JPM could easily be trading at $64/share. Again, this goal is not a stretch target by any means and the earnings walk shows that this EPS is achievable without any major economic recovery or anything like that. If JPM traded at 15x p/e, the stock could easily get to $96/share. I know it seems ludicrous to think that a financial company can trade at a 15x multiple as people are still suffering from a sort of post-crisis syndrome, but I think people may be surprised. Don't forget, it wasn't long ago that bank stocks traded at 2-3x book. Markets do change.

- The first chart above shows how well JPM is managed, growing book value per share through the crisis at a healthy pace. Dimon thinks they can earn at least 15% on tangible equity and I did say last fall that tangible book value per share is a no-brainer buying opportunity because of that 15% floor in returns (that they actually achieved even in bad times). Their ROE too is above 10%. The return on equity for the last five quarters were: 11%, 13%, 12%, 9%, 8% and the return on tangible common equity was 16%, 18%, 17%, 13%, 11%. And this was when banks and investment banks aren't supposed to be doing too well.

- So from the above, we can say that tangible book value per share is a really cheap level for JPM shares and one can easily argue that it is worth at least book value per share, which is $46.59/share from the above chart. It's now trading at under $40/share, so is trading at a 14% discount to that.

- Wells Fargo too has low double digit returns on equity (9.9%, 10.3%, 12% for the years 2009, 2010 and 2011) and trades at 1.3x book value per share. If JPM traded at a simliar 1.3x book value per share which I don't think is unreasonable or aggressive at all, that would put JPM stock at $61/share. That's 50% higher than where it is trading now.

- I think the market doesn't like banks now for obvious reasons, and they also really dislike investment banks as they think the model is dead. But JPM has proven and is proving that they can make money and good returns in the business. Over time, I think people will get over this fear and the market will increase the valuation of JPM closer to Wells Fargo.

- So either way you look at it, at 10x the $6.40 normalized EPS or 1.3x book value, you can get to JPM trading at $60+/share without being too aggressive.

- The caveat, of course, is that this is a financial stock so a total blowup in Europe or a deeper recession in the U.S. would cause all financials to sell off. A prolonged low interest rate environment as in Japan can keep up downside pressure on net interest margins too, so this is not without risk.

- As usual, if you are interested in JPM, check out the slides at the JPM investor relations website and do your own work!